SoFi: Bank To The Future

Super-App Superpowers, Becoming A Bank, and Galileo the Alchemist

Welcome to the 195 new and curious minds who have joined The Operator since October 19! If you are reading this but have not subscribed, join 1,045 dapper and well-regarded others by subscribing here:

Happy New Year 👋

I begin to write the present piece from the familiar sanctuary of a well-worn couch, stuffed and hungover – not from tipple but from turkey. After glancing sideways at a beleaguered portfolio this morning, it’s hard not to crave a comforting fortress such as this. November and December have been smacking growth companies around, despite fantastic Q3 numbers. It can be challenging to remain confident and hold in times like these, particularly fintech companies like SoFi.

I wish I could tell you I had a dream – one in which SoFi CEO Anthony Noto drove up in an electrified DeLorean with a ‘GAL1LEO’ vintage plate. That he strode out of butterfly doors wearing Solana stunners and an LA Rams helmet to tell me SoFi is the bank of the future — that, “Where we’re going we don’t need roads.”

But that didn’t happen.

This visual, while artificial, can still remind us why we invest in the first place. Disruptive technology companies allow people like you and me to invest in our dream of future. And in my opinion, being a partner in the big, transformative ambitions of these companies makes the wild ride worth it. So does the upside.

But to not get shaken out of these iconic names – to weather sell-offs, FUD and FOMO – requires conviction. And outside a natural aptitude for strong opinions, the only way to build conviction is by understanding the thesis. That’s what I do. If conviction were a muscle, I’m your Cody Rigsby.

So today, as we venture out into a bold new year, we both revisit and rebuild the investment thesis for SoFi Technologies. After all, few companies have a roadmap more ambitious, a CEO more forward-thinking, than SoFi.

SoFi has aspirations to build the financial super app — a platform never before seen in the Western hemisphere. If effected, SoFi will boast a potent blend of SaaS-margin revenue and the lasting power of a bank. Sound compelling?

Trading at just $12 Billion in market cap today, and down roughly 50% from all time highs, I think so.

Let me show you why SoFi is one of my core conviction picks over the next 3 - 5 years.

SoFi: Three Legs, One Platform

In my previous SoFi article, SoFi: David Becomes Goliath, I explored SoFi’s founding mythology from Stanford Graduate School of Business to ignominious founder exit. From the arrival of CEO Anthony Noto to Chamath-hyped SPAC merger. I also outlined SoFi’s three business segments: lending, technology (Galileo), and financial services. If you’re unfamiliar with SoFi’s business model, please start there.

SoFi Lending

Lending is SoFi’s largest, most mature, and most profitable segment, and includes student loan refinancing, personal, and home loans. Although SoFi began as a strictly student loan refi business, today that segment constitutes only 22% of SoFi’s revenue, with home and personal loans constituting the remaining majority.

This revenue diversification is critical, with recent events providing a compelling rationale. Since the start of COVID-19 the federal government has placed a pause on student loan payments — slashing demand for refinancing.

Galileo: Infrastructure-as-a-Service (IaaS)

Galileo is SoFi’s technology platform, which provides fintech IaaS to the majority of the world’s neobanks, including Robinhood, MoneyLion, Dave, Chime, Varo, Revolut, Monzo, Klar and Transferwise. SoFi acquired Galileo in April, 2020 for $1.2 Billion.

Galileo is considered the API standard for card issuing and digital banking, offering sophisticated payment card programs and backend digital banking services.

SoFi Financial Services

SoFi’s nascent financial services segment includes a rapidly growing number of products on a unified dashboard. These are each high-frequency, top of funnel products used to onboard members and get their “money right.”

SoFi: Q3 2021 Tale Of The Tape

On November 10, 2021, SoFi announced stellar Q3 2021 financial results, including a beat and raise. Revenues grew by 28.4% to $278.3 million on the back of tough Q3 2020 comparisons, an upside surprise of nearly $30 million. Adjusted EBITDA came in at $10 million, a $12 million beat at the midpoint of guidance, and SoFi’s fifth consecutive quarter of positive adjusted EBITDA. Management forecasted an acceleration of growth in Q4 and raised both full-year revenue and adjusted EBITDA guidance.

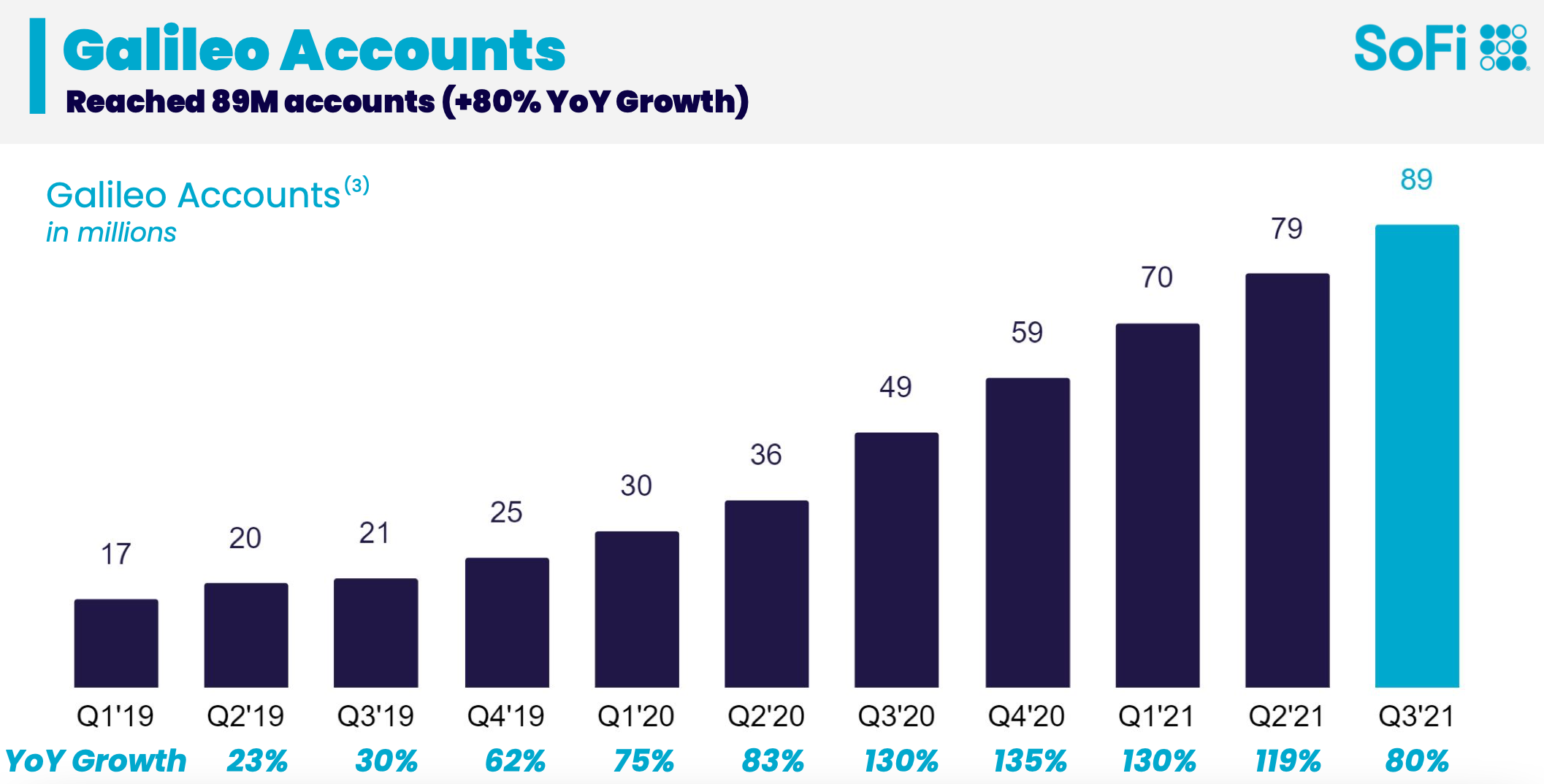

SoFi added 377k members in the quarter for a total of 2.9 million, and Galileo accounts reached 89 million, growth of 80% year over year. Despite student loan refinance headwinds, SoFi’s lending division posted another record quarter, leaning on strength in personal and home loans.

SoFi’s net income for the quarter was -$30 million, a stark improvement from -$177.6 million and -$165.3 million in Q1 and Q2 2021, respectively. This was driven in part by record contribution profits of $93.9 million.

As you can see, lending and, to a lesser extent, Galileo, are footing the bill for the rapidly growing and currently unprofitable financial services segment.

SoFi guided for full-year revenues of $1.002 - 1.012 Billion, growth of 62% at the midpoint, as well as 43% revenue CAGR through 2025, including 53% in 2022. This guidance makes SoFi the fastest growing blue-chip fintech I’m aware of.

Financial Super App: The Theory of Everything

From a 30k foot view, SoFi is a rapidly growing, diversified fintech company, funding growth in its incipient technology and financial services divisions with lending profits. You may have heard this amalgamation affectionately dubbed a “one-stop shop,” or, a “super app.”

The original super app appellation came from BlackBerry founder Mike Lazaridis back in 2010. He described it as:

“A closed ecosystem of many apps that people would use every day because they offer such a seamless, integrated, contextualized and efficient experience.”

If we look East to China, mega-caps Tencent and Alibaba have built empires on top of their own super apps, WeChat and Alipay, respectively.

Source: Visual Capitalist

On the WeChat app, users can not only engage in social media and make mobile payments, but also complete all esoteric acts of commerce imaginable, such as ride hailing, charity, and game token purchases. Because people never need to leave the app, they never do.

A confluence of technological and regulatory circumstances led to the rise of the Chinese super apps. While we may have more valuable companies in the United States, we have nothing so utterly pervasive as a WeChat or Alipay.

And yet, that’s what SoFi aims to build. Well, a version of it. SoFi is indeed attempting to build a super app, but in a less monopolistic, free-market flavor.

In its final form, SoFi hopes to become an aggregator of each of life’s consumer-facing financial products, to help its members achieve financial independence. Something decidedly between a bank and a WeChat — a financial super app. If they can pull this off, SoFi might unify the 15 distinct finance apps on my phone into one, high-walled garden of commerce.

But SoFi must race to make this happen, as it’s not the only company pursuing this opportunity. Over the past year the most iconic names in finance have trumpeted ambitions to architect the same concept, using different vocabulary.

As a matter of fact, Robinhood, Coinbase, Block, PayPal and Affirm are all vying for super app status:

“We look forward to being our customers' single money app…”

-Robinhood S-1

“So there's a ton of things that can happen with kind of super apps going forward. We clearly will be a player in that. We will clearly be a market leader in that.”

-Dan Schulman, PayPal CEO, JPMorgan 12thAnnual U.S. All Stars Conference, September 2021

“Our goal is to become the primary financial account for our retail users and the one-stop shop for institutions’ crypto asset investing needs.”

-Coinbase S-1

-Block September 2021 Investor Presentation

Probably nothing.

But seriously, is super-app just another buzzy futurism-in-vogue, like metaverse, AI and Web 3.0? I don’t think so.

Truthfully, I believe the company that builds an actual, honest-to-goodness financial super app will become the first trillion dollar consumer-facing financial institution in the free world.

Here are the 3 reasons why building a super app breeds fintech superstardom:

1. Cross buy CAC flows to profits

2. Data advantage powers safer underwriting and product offering

3. Diversified business = flexibility = resiliency

1. Cross buy CAC flows to profits

Let’s get into the weeds a bit.

Long-term value (LTV)/customer acquisition cost (CAC) is a basic metric of unit economics for consumer financial services. In other words, how much revenue a customer generates divided by the cost to acquire that customer. Each financial product (and company) has its own CAC and LTV.

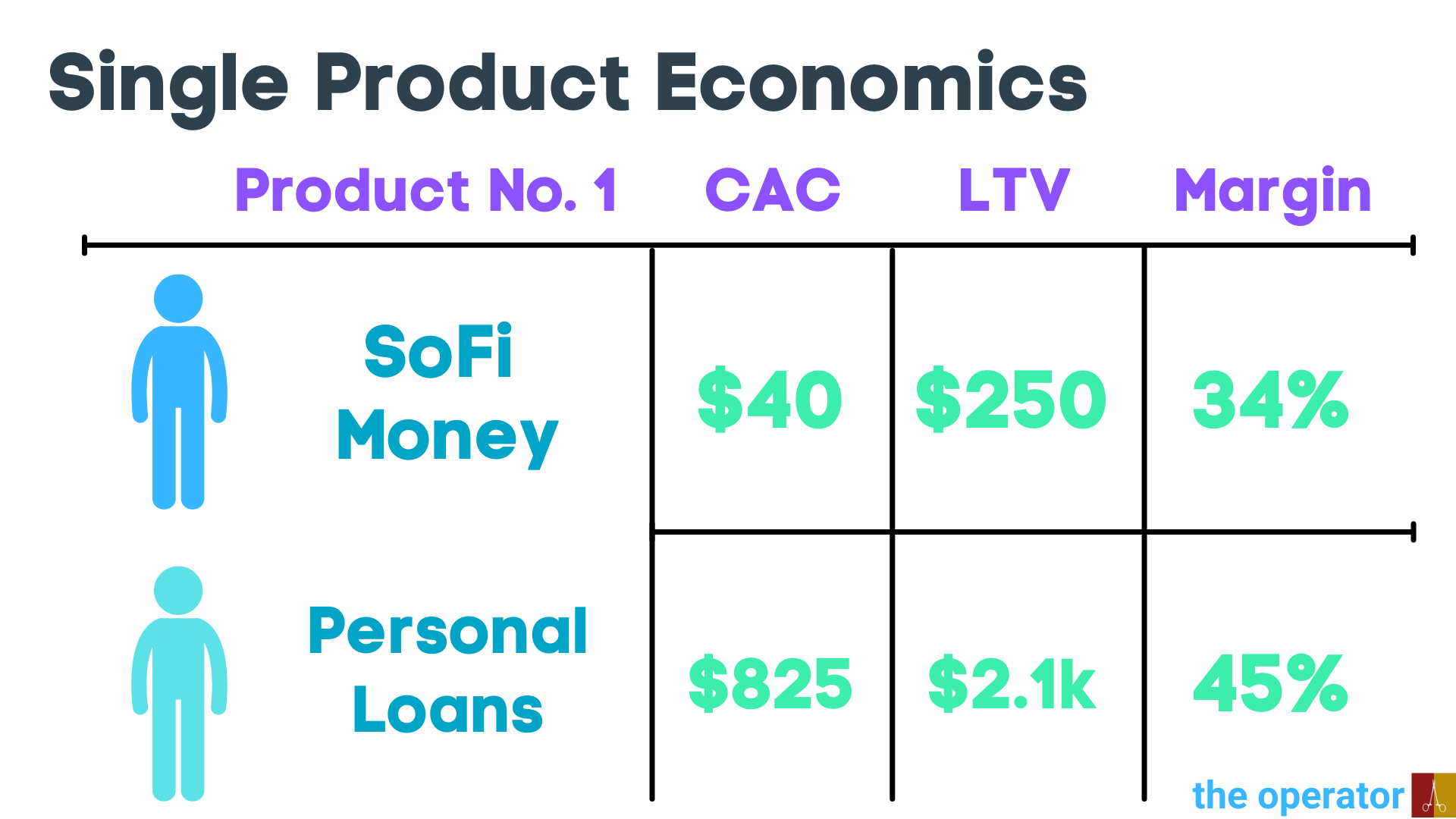

For example, SoFi might acquire a new member for its SoFi Money product (checking/savings account) at a CAC of $40, and a Money user generates ~$250 in revenue (LTV) over 5 years.

But what if that SoFi Money member purchases a second product (ie, “cross-buy”), such as a personal loan? Although SoFi’s personal loan CAC is traditionally upwards of $825, SoFi pays no CAC for products 2 – 10; it only pays to acquire the customer once. So when a SoFi Money member takes out a personal loan, that $825 of CAC is absorbed as pure profit.

Cross-buy is the superpower of the super app.

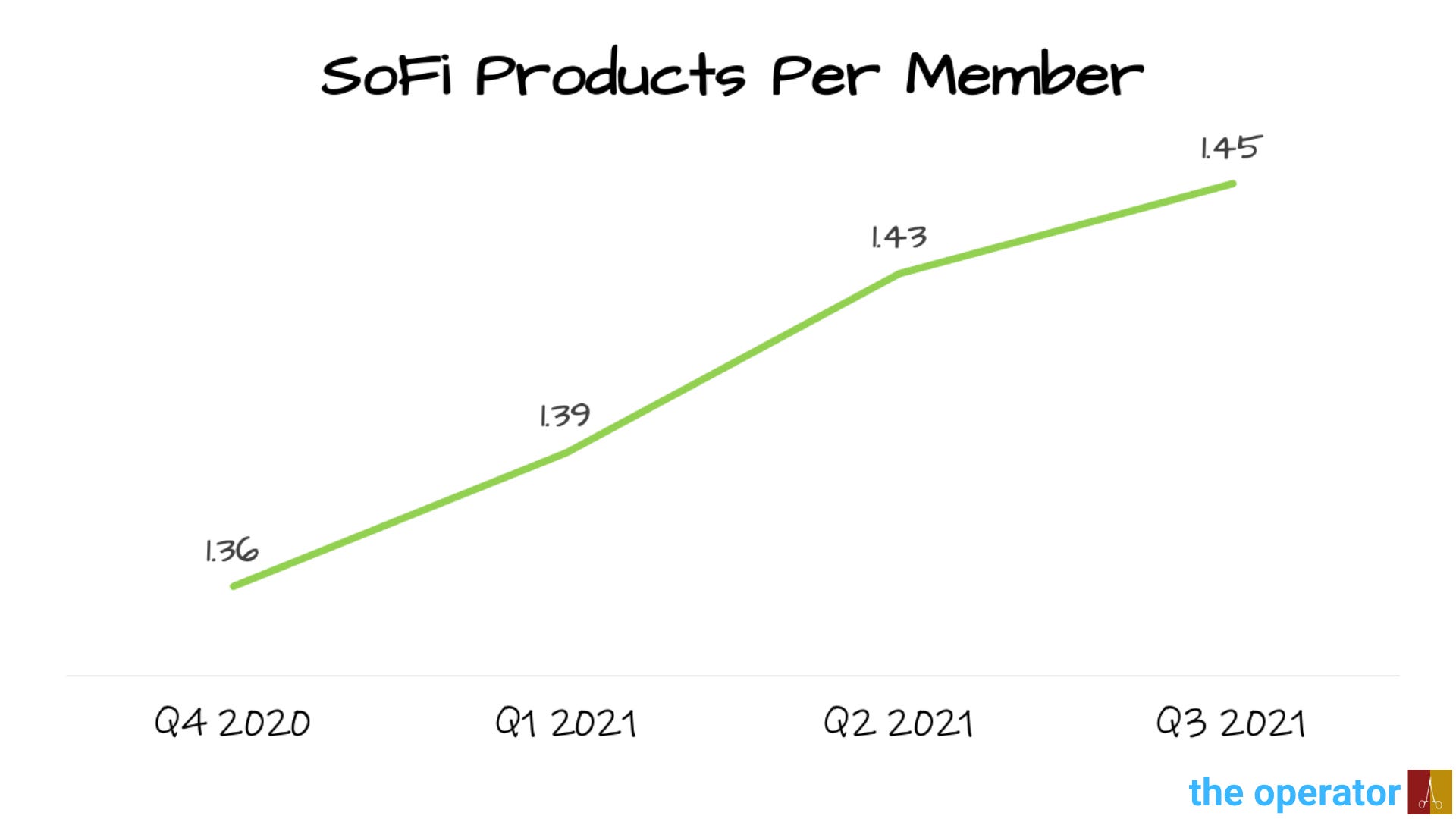

And SoFi has managed to grow the all-critical cross-buy metric of products per member (PPM) each quarter despite more than doubling members over the past year. In fact, Q3 was SoFi’s highest ever for cross-buy, posting 1.45 PPM, and products have increased 2.8X over the past twelve months.

By harnessing cross-buy to divide CAC between products, SoFi maximizes profitability without having to charge members more in fees. It’s no coincidence that with super app economics, both the company and its members, win.

But there’s a crucial nuance to SoFi’s model. Because CAC’s vary by product, cross-buy economics are much stronger if member acquisition begins in the financial services segment (~$40 CAC, 86% profit margin) rather than the lending segment (~$825 CAC, 45% profit margin).

In fact, the difference in margin is nearly double.

So not only is cross-buy important, but directionality is as well.

Through its financial services division, SoFi is building a suite of products that combine high-frequency usage and low CAC as top of funnel to direct members towards high LTV/high CAC products, like lending.

And the strategy of controlling cross-buy directionality is working beautifully. In Q3 2021, SoFi Invest, Money and Credit Card-first members drove a record 79% of new member growth, and 73% of cross-buy. This type of execution allows SoFi to achieve margins north of 80% in many cases, higher than your favorite SaaS company.

Can Wells Fargo say that?

2. Data advantage powers safer underwriting and product offering

There’s an under-discussed data advantage to the super app model and it’s remarkably powerful.

SoFi is able to assemble a complete financial picture of its members — credit score, spending, saving, investing, loan payments, credit card balance, etc. Every daily check-in and purchase informs SoFi’s risk modeling. By capitalizing on this data advantage, SoFi is able to both offer lending products in a timely manner AND underwrite them more safely.

Noto highlighted this opportunistic approach to data finance on the Q3 earnings call:

“Often is the case that we'll see that someone through Relay has a number of credit cards that are fully utilized and we can offer that person…a lower-cost term loan through our personal loan business.

Or we could see someone with a lot of excess cash in their SoFi Money account, and we could offer that person a free certified financial planner session to help them invest that money and have it compounding over years.”

The super app model grants SoFi an intimate understanding of its members, which allows the provision of increasingly useful services, higher cross-buy, and lower default rates. Each of these features drives the other forwards.

These data are also being used to formalize more rigorous credit metrics.

Although FICO scores generally track loan default rates well, they are by no means perfect models of financial health. Traditional credit scoring utilized by banks analyze dozens of variables to safely underwrite loans with acceptable default rates. But by having visibility into a member’s complete financial footprint, SoFi is able to aggregate thousands of variables.

SoFi’s data aggregation can identify pockets of individuals who do not meet traditional credit standards but actually have similar default risk profiles as those with higher FICO scores. This broadens the addressable market and lowers default rates compared to incumbent lenders.

I actually do not cover another company with this type of advantage. It’s remarkably powerful to have a platform where customer activity informs marketing of ancillary financial services that can be offered at lower risk.

Risk management is a critical aspect of financial services, and the super app model offloads risk by design. Future product launches such as tax preparation and insurance expand the ecosystem, yes, but more importantly, feed high quality data back into the system to fuel the super app virtuous cycle.

The super app model eliminates roadmap ambiguity.

As SoFi’s platform scales, it is able to build and shape products based on freely sourced feedback. This eliminates product roadmap guesswork, makes for efficient marketing spend, and allows SoFi to constantly build products members crave.

This sure-footed agility has resulted in the launch of SoFi credit card, IPO investing, early paycheck, auto loan refinancing, and weekly dividend ETF products in 2021 alone. And in the capricious crypto space, SoFi has similarly managed a high velocity of innovation.

The SoFi Crypto platform recently added seven new cryptocurrencies including Uniswap, Cardano, and (my favorite), Solana. Meanwhile Robinhood has added only four coins since 2018, PayPal offers four total, and CashApp (Block) only allows trading of Bitcoin (Come on, JD).

And there’s no sign of product launch deceleration in sight for SoFi. Noto has remarked several times the team is working on two products members have clamored most loudly for: options trading and margin trading. Both of these products are available to Robinhood’s 20+ million users and widely used. I have reason to believe tax management and insurance are the next products on SoFi’s launch schedule, and that the former will be available prior to tax season.

Finally, as member data is already integrated into SoFi’s platform from first product sign up, these ancillary products can be offered and purchased with the tap of a button – no prolonged application process. Loan applications offered and secured within minutes.

This is a subtle feature, but frictionless checkout is sliced bread for e-commerce and fintech’s alike. Nobody likes entering all their financial information into a multitude of apps. Nobody likes applying for anything.

With each new product signup, SoFi members are treated like a virtual regular, which engenders trust and ecosystem loyalty.

3. Diversified business = flexibility = resiliency

For advantage #3, we’ll discuss super app flexibility, resiliency, and SoFi’s positioning amongst pure-play peers.

In 2022, interest rate hikes will impact each and every American financial institution. But few of these institutions are diversified enough to turn negative macro events into a net neutral, or even net positive. For example, a low interest environment benefits home loan and student loan refi, as well as investing appetite and growth stock valuations. But in a higher interest rate environment, demand for personal loans rises, and banks and fintechs can earn more on digital banking spreads. Although the axis of opportunity shifts, SoFi will remain in a position of strength. This is the hallmark of a resilient, lasting financial institution.

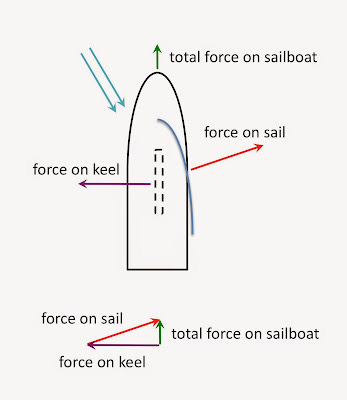

As a brief aside, I recently found myself studying the physics of sailing (no reason). Prior to this, I assumed sailboats could only travel away from the direction of wind. I surmised that if the wind was blowing from the direction you wanted to go, it was time to pick a different direction. But I was fascinated to learn that a sailboat is actually able to leverage a powerful submerged component, the keel, to redirect force and cruise against the wind.

In fact, a well-built sailboat can fly even faster than its headwind.

Source, Credit Tamela Maciel.

The invention of the keel revolutionized sailing, and made the open ocean and the opportunities it guarded, navigable.

Pure play businesses like Robinhood have a binary approach to tailwinds and headwinds, much like a rowboat. If trading volume and crypto interest is high, Robinhood chugs along at a merry pace. But should trading volume and crypto interest drop (see Robinhood’s Q3 earnings miss and resulting stock price implosion), good luck getting back to safe harbors.

But a diversified financial institution, like SoFi, can flex and pivot in different economic climates, turning headwinds into tailwinds, like a sailboat. Even throughout 2021 — a year in which SoFi’s largest book of business, student loans, was slowly suffocated by a federal pause — SoFi managed to beat and raise its own aggressive guidance by leaning on strength in personal and home loans. As Galileo and SoFi’s financial services division continue to gain strength and scale, product revenue concentration disperses, which will only improve SoFi’s posture for the dynamic landscape ahead.

And yet the stock does not adequately price these attributes. In fact, if you break out valuations for SoFi’s lending, financial technology and financial services segments, you find SoFi trades at a steep discount to its pure play peers.

As a valuation exercise, I constructed a fictional company composed of SoFi’s standalone competitors, including Upstart, Marqeta and Robinhood for SoFi’s lending, financial technology, and financial services divisions, respectively. Before you quibble with my choices, if these three companies merged today the union would eerily resemble SoFi, albeit 3X larger.

After much thought, I decided to name this fictional company “Hans Gruber.” There are many excellent Christmas antagonists to choose from, but I challenge you to do better than the late, great Alan Rickman in Die Hard (which IS a Christmas movie btw).

Here’s what I uncovered:

2021E = 2021 Estimated, P/S = Price/Sales

And if we apply Upstart, Marqeta and Robinhood’s P/S multiples to SoFi’s lending, fintech and financial services businesses, respectively, we arrive at the following valuation:

Granted the multiples of Upstart, Marqeta and Robinhood, SoFi would be valued at $15.6 Billion. But it’s not.

Trading today at $12 Billion, SoFi’s three business lines are undervalued compared to pure play peers by nearly 30%. Not to mention SoFi is already down 35% over the past two months after a solid Q3 beat and raise.

How is that possible?

We’ve already discussed why SoFi merits a premium over these standalone offerings. SoFi’s super app model will perennially provide superior unit economics, data-driven marketing, and safer underwriting than peers. A multi-product SoFi member generates LTV/CAC multiples much higher than standalone offerings like Upstart, who don’t have the benefit of cross-buying to slash CAC and multiply LTV. And SoFi’s diversified product portfolio means it can turn any macro climate into a tailwind.

With a rapidly expanding product suite and well-governed cross-buy directionality, SoFi is the closest American fintech to super app nirvana. This clearly merits a premium to the loud-talking laggards and pure play peers we’ve discussed.

But market inefficiency is our opportunity, after all.

If CAC Is The Superbowl of FinTech, Then SoFi Is Hosting The Superbowl

Now that we’ve outlined the advantages of the super app model and why each member of the fintech royal family pursues it, we can dive deeper into SoFi itself.

If you’re familiar with my work, you’ll know I’m a stickler for unit economics. For SoFi in particular, I’ve been tracking what I believe is the most important growth metric in fintech since the day IPOE turned into SOFI: customer acquisition cost.

CAC is a simple statistic but represents a blend of key performance indicators, including marketing efficiency, growth, and operational execution. Mathematically, it’s the denominator of the LTV/CAC equation, and therefore bears the greatest impact on a company’s unit economics. And as good as the super app model is, it’s early days, and SoFi has historically been unable to compete on CAC with the 800-pound gorilla similarly chasing financial revolution: Block.

I wrote previously SoFi enjoys $40 CAC for most of its financial services products. This is excellent considering LTV’s for cross-buy members ascend to thousands of dollars. For reference, incumbent banks traditionally spend around $1,000 per customer acquisition. But CashApp, Block’s peer-to-peer (P2P) payment and investing platform, has posted CAC’s as low as $5. Gulp.

Block CEO Jack Dorsey is a media wizard, leveraging his deep marketing experience as founder and (now) former-CEO of Twitter to launch viral campaigns such as #CashAppFriday to drive cost-efficient sign-ups. CAC is how Dorsey’s dongle became a sprawling fintech empire.

When I last wrote about Block in June 2021, I expressed concern that SoFi was not generating similar marketing efficiency.

Here’s what I wrote in my article Square: Winner Takes Most:

“The holy grail of the fintech space is low customer acquisition cost. Dorsey’s mastery of viral social media advertising generating low CAC's has been a primary catalyst of Square’s titanic growth rates…

As a SoFi shareholder and bull, I was disappointed to learn in my research that SoFi has been unable thus far to creatively turn its Twitter presence into a customer acquisition engine. Despite 120k+ followers, the SoFi Twitter page has relatively low engagement and no promotional activities reminiscent of #CashAppFriday.

SoFi CEO Anthony Noto coincidentally was formerly COO of Twitter when #CashAppFriday first launched, and I believe he will be able to leverage this experience into a more engaging social media presence.”

Six months have passed since I wrote that, and CEO Anthony Noto, former Westpoint linebacker, Green Beret and Wharton grad, did not take my challenge lying down. In fact, Q3 was an inflection point for SoFi, as a confluence of circumstance and positioning drove wildly efficient member acquisition.

Here’s a direct Noto quote from the Q3 earnings release:

“During the third quarter, we launched a series of marketing campaigns designed to increase SoFi’s brand awareness, members and products.

The SoFi Money Moves brand campaign we debuted during the US Open tennis tournament in September and the regular NFL season has significantly raised SoFi's profile. This campaign includes an integrated, cross-platform, multi-channel marketing program that leverages nationally televised NFL games and events at SoFi Stadium, our most comprehensive digital influencer program to date, a SoFi Money Moves social video contest on TikTok, and a new referral program.”

Noto accomplished exactly what I challenged him to, and then some.

In Q3 SoFi’s unaided brand awareness more than doubled, and TV spots drove 500+ million impressions. SoFi’s version of #CashAppFriday — #SOFIMONEYMOVES — was used over 1 million times on TikTok and received more than 8 billion views.

These campaigns were galvanized by the advent of the NFL regular season and two dynamic teams playing high-octane football in the palatial SoFi Stadium. In fact, games played at SoFi stadium, on average, receive almost 30% more viewers than games played anywhere else. Meanwhile high profile entertainers such as The Rolling Stones, Justin Bieber and BTS have recently performed at SoFi stadium.

Perhaps what I was most excited to see was SoFi’s Q3 partnerships with Pomp and Packy McCormick of the Not Boring newsletter. Pomp’s crypto podcast is excellent, and reading Packy’s newsletter was the reason I began writing about finance in the first place (and if you haven’t read Not Boring, you should do that now) . Between these two gentlemen SoFi is generating an atmosphere of highly esteemed, triple-distilled, influence — the stuff that drives member sign ups and goodwill.

And if the Super Bowl of fintech is CAC, SoFi is hosting the Super Bowl. That’s right, on February 13, 2022, Super Bowl LVI will be held at SoFi Stadium in Inglewood California. The halftime show will feature Dr. Dre, Eminem, Kendrick Lamar, Snoop Dogg and Mary J. Blige. CAC catalysts abound.

If I were grading SoFi’s marketing efforts against fintech peers, SoFi just set the curve. Cheers to you Mr. Noto.

Were Galileo An Alchemist

In Unity Software: The World Engine, I described the sustainable advantages of building infrastructure for a given space, which I called ‘owning the middle.’

“There is something compelling, something inevitable about becoming the gatekeeper of the path everyone must pass through.”

Galileo, SoFi’s technology division acquired in 2020 for $1.2 Billion, represents best-in-breed infrastructure, rapidly gaining ubiquity in the fintech space.

Source: SoFi Q3 2021 Earnings Presentation

Galileo is primarily a payment processing business by revenue, earning fees on transactions, and counts 90% of all neobanks as customers. Each time one of the 90 million Galileo-powered accounts swipes a card, Galileo earns a cut.

Although Galileo account growth exploded in 2020 and 2021 (106% 2-year CAGR as of Q3 2021), revenue growth has been a more pedestrian 30%. But I believe account growth is a harbinger of revenue growth to come.

“A big focus of ours over the course of the last year and a half has been on stabilizing the platform and setting us up for scale and real growth. We've made significant investments in terms of transitioning from on-prem and into the cloud.

Over the course of the next several quarters and throughout 2022, you'll start seeing us get into additional products and features that will help drive ARPU and real customer growth.”

Chris Lapointe, SoFi CFO on Galileo, 25th Annual Credit Suisse Technology Conference

SoFi has spent the past 15 months migrating Galileo to the cloud. As a result, in 2022 and beyond, SoFi will be able to launch new products more cheaply, with greater agility, and at greater scale. Investment in this transition has slowed 2021 product roadmap for Galileo, but now that this transition is complete, I expect unfettered product and revenue growth ahead.

But why did SoFi acquire Galileo in the first place?

For the past year, I’ve wondered what the true value of Galileo is to SoFi. Obviously having a rapidly growing and profitable financial technology segment in-house is compelling, and frankly, $1.2 Billion was a steal (just look at Marqeta’s 20X multiple). But I questioned how Galileo fit into the super app strategy. It required me to take the time to write this article to truly understand the Galileo puzzle piece.

Put plainly, the SoFi app is a digital shelf where all future Galileo products are on display.

Account set-up, funding, direct deposit, ACH transfer, IVR, early paycheck, direct deposit, bill pay, transaction notifications, check balance, and point of sale authorization — every frictionless SoFi feature that generates happy consumers is actually an API hosted by Galileo.

For example, SoFi’s reward feature, which rewards members with points (1 point equals 1 cent) for activity — such as daily log in, direct deposits, or reading an article about a stock — is software coded by the Galileo team. This software was built by Galileo for SoFi, but in 2022 I believe Galileo will productize this functionality to its many neobanking customers, alongside credit processing, fraud management and lending-as-a-service.

This is an incredibly powerful advantage for the super app model SoFi pursues. Galileo builds the software infrastructure for each of SoFi’s financial products, and then sells that software to other fintech companies. SoFi is both customer and purveyor, double-dipping on profits. And because all the software was written by Galileo, each API communicates with the next seamlessly — these are features that actually work better together.

Many people believe SoFi’s financial services division, the app dashboard, represents the super app. But it’s not. SoFi the company, is the super app, and Galileo is the keystone. Block and Robinhood are excellent companies, nipping at SoFi’s heels in the super app race. But these companies must dump R&D dollars into API’s for the dozens of financial products they must add to compete. That is the cost of doing business. With Galileo, new API’s are built to improve SoFi member experience AND become software products sold to a captive audience of 89 million accounts that are currently under-monetized.

If you’ve ever heard Galileo referred to as the “Amazon Web Services (AWS) of fintech,” this is why. AWS offers over 225 global cloud products to nearly every business in the world, and is considered the pinnacle of operating profitability. Most of AWS’s products were developed in-house to improve customer experience.

It’s by converting B2C features to B2B products that the actual alchemy happens.

The B2C features improve user experience and choice, driving growth. But the resulting B2B products cost nearly nothing to build, and like all software can be infinitely scaled, driving profits. And as more products are added to the ecosystem, the flywheel’s orbit broadens, like the rings of a planet. For competitors entering the super app race, the question increasingly becomes — “do you want to front the costs/time to write dozens of API’s, or do you want to just set up an account with Galileo?” Robinhood and the majority of the world’s neobanks have already answered this question, and therefore their profitability will never measure up to SoFi’s.

None of SoFi’s super app peers have this advantage, this ‘AWS of fintech’ call optionality, and it’s core to my thesis.

Bank To The Future

There’s a catalyst in the ether that completely rewrites SoFi’s future: approval of the bank charter.

If you follow SoFi, no doubt you’ve heard numerous others speculate on the timing of approval, or read conspiracy theories based on the prior timelines of Block or Lending Club. I have no idea when this will happen, refuse to speculate, but I 100% agree the bank designation will be transformative.

It might seem odd that a fintech storming the stagnate beaches of JPM and Wells Fargo would pursue the defender’s strategy. But becoming a bank allows SoFi to ascend to the final form of its evolutionary tree. And that maturity equals profitability.

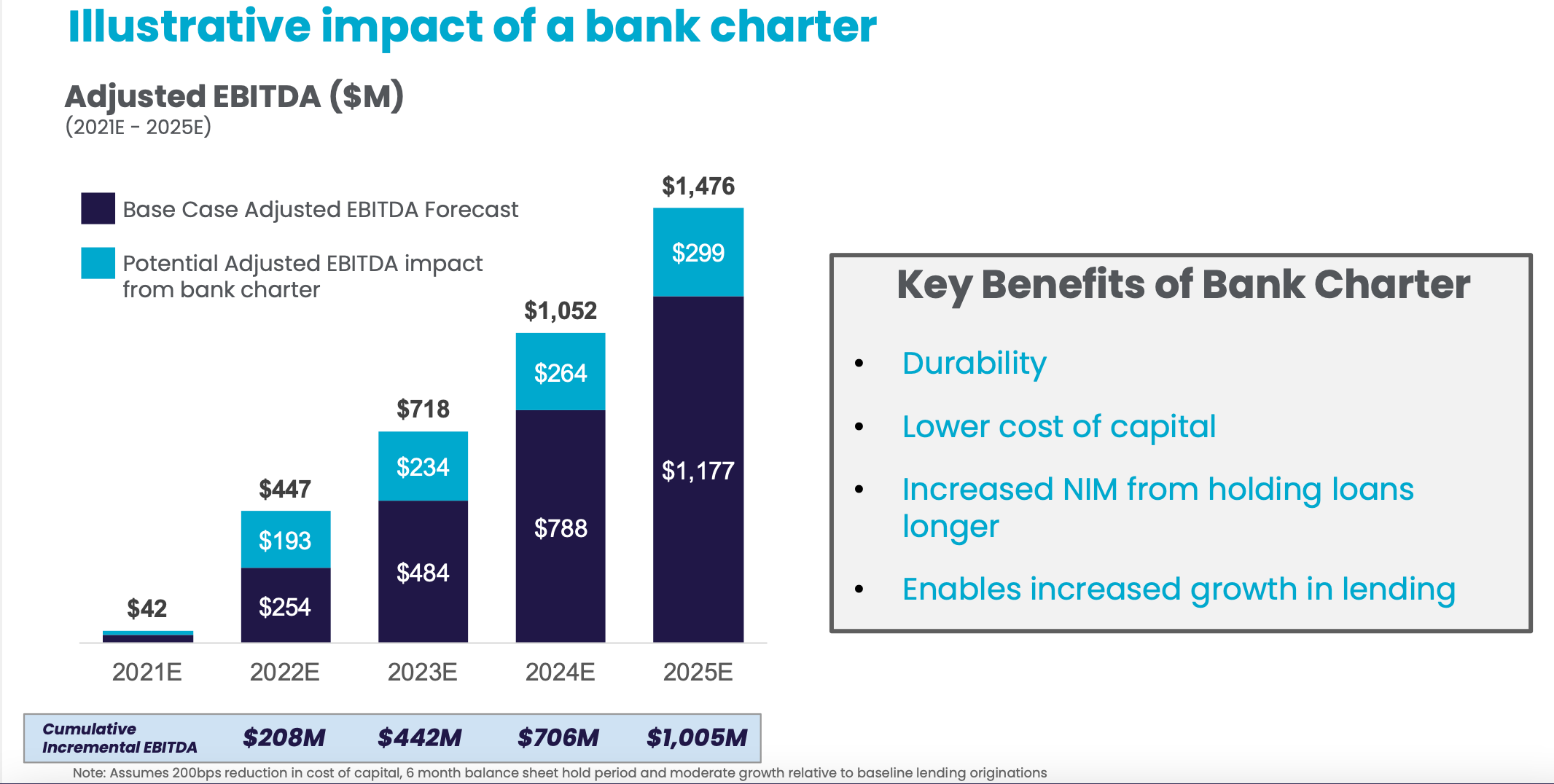

Source: SoFi Investor Presentation

As someone who writes exclusively about disruptive tech I rarely get the opportunity to discuss profits, so I embark on the following section with glee. In SoFi’s original investor presentation, management cited the bank charter would yield incremental EBITDA of > $1 billion by 2025, including $193 million in 2022 alone.

For growthy tech companies, profitability multiples such as enterprise value (EV)/EBITDA are considerably larger than revenue multiples like P/S. For example, today Upstart has an EV/EBITDA multiple of 156. Hypothetically, if we apply that multiple to SoFi’s 2022E earnings, the bank charter (+ $193 million) would raise SoFi’s enterprise value by $30 billion.

Now, as $30 billion is roughly 2X SoFi’s current EV, I’m not claiming the bank charter would catalyze a 200% rise in stock price. But it would add considerable weight to the argument that SoFi is not receiving the valuation it merits.

How does the bank charter structurally change SoFi’s business?

I wrote before that cross-buy is the superpower of the super app. But a bank charter makes a super app something more — something durable, defensible, and lasting.

SoFi currently relies on $6 billion in warehouse capacity alongside its own equity capital to fund lending originations. On average, SoFi pays 3%, or 300 basis points (bps) to originating partners to lend capital to its members. But with the charter, SoFi will be able to use its own members’ deposits to originate loans like a bank, which means those 300 basis points in capital costs are eliminated.

While SoFi will inevitably enjoy some of these saved bps as profits, I believe they will actually redirect most towards continued growth. For example, following charter approval, SoFi will likely increase APY for SoFi Money members, which will drive both member growth and higher deposits (AUM), increasing the amount of loans SoFi can self-originate.

Additionally, those bps can be redirected towards lower interest rate loans for members, which makes SoFi’s lending products more competitive, driving growth here as well. Even if SoFi spent 75 bps increasing SoFi Money APY (currently at 0.25%), and 100 bps lowering loan rates, 125 bps would remain for profit-taking.

In the last twelve months (LTM), SoFi has originated a total of $11.2 billion in loans. A 125 bps capital cost improvement raises LTM EBITDA by $140 million, or 3.75X SoFi’s LTM adjusted EBITDA. This is significant.

As the cherry on top, remember that cross-buy allows SoFi Money-first members who purchase a personal loan to generate astronomical profit margins of 86%. With the bank charter, SoFi will be able to lend that member his/her own money (as well as the money of other members) as the personal loan, at zero cost, likely achieving margins of 90% or better.

This is absurd profitability for any company, let alone a financial services company.

Once the bank charter is secured, the nexus of strategy shifts to SoFi Money, and specifically, direct deposits. Where you direct deposit is where you bank. I expect customer acquisition to focus on driving sign-ups for direct deposits in SoFi Money accounts, given the advantages of rising AUM for SoFi’s growth and profitability aspirations. As more and more members add direct deposit, activity on their traditional bank apps will dim, and eventually, go dark.

Student Loan Refi Landscape

Before we wrap up, I’d like to highlight a recent negative catalyst.

One of SoFi’s headwinds since the emergence of COVID-19 is a federal moratorium on student loan repayment. There’s not much demand for student loan refinancing when your student loan repayment is paused, after all.

As student loan refi was once SoFi’s largest book of business, this is a headwind worth monitoring. In August 2021, President Biden pushed back the pause through January 31, 2021, and this was believed to be the final extension of debt relief — marking a massive catalyst for SoFi in February, 2022.

And then Omicron happened. I had originally titled this section “SoFi’s 2022 Student Loan Refi Bonanza,” and was planning to highlight a massive surge in this business going into the new year. But on December 22, 2021, the Biden administration again extended the student loan pause through May 1, 2022.

This recent bit of news puts a bit of a damper on what I previously expected to be eye-popping Q1 2022 growth and profitability guidance. But there might be a few kernels of optimism for those who know where to look.

First, provided student loan debt is not canceled altogether, refi demand is not diminished, but simply pushed back. Assuming no further pauses, Q2 - Q4 will be magnificent quarters for SoFi’s lending division, a bonanza indeed.

But perhaps even more importantly, we return to issue of cross-buy directionality. Today SoFi is in aggressive customer acquisition mode, massively expanding the ecosystem to the tune of 300,000 - 400,000 new members per quarter through its low CAC, top of funnel financial services division.

Had there been no further pauses, in January many SoFi members would have likely refinanced their student loans, at a CAC of $0. But many others would have come to the SoFi platform for the first time, purchasing a student loan refi product at traditional (high) acquisition costs, swimming against the current of cross-buy directionality, generating middling margins.

The longer student loan repayments are paused, the more time SoFi has to onboard and form relationships with new members through its low-CAC channels — the more opportunities SoFi has to learn about its member’s debts and student loan rates. So when the music finally does stop, more SoFi members can be cross-sold student loan refi products at bargain basement acquisition costs to SoFi.

As this pause extends now to May 1, 2022, the potential energy of profitability for SoFi quietly expands alongside it.

While I don’t believe student debt will be forgiven altogether, there’s no way to know. Similarly, there’s no way to know if May 1, 2022 will truly be the final day of the pause. These are headwinds to track, but the underlying economics of pause extension are less sinister than previously expected.

As a final note, student loan refi comprises only 22% of SoFi’s revenue today, and that number continues to shrink on a quarterly basis. If the Biden administration attempted to erase student debt altogether, it would be a marked negative for SoFi’s growth story, but not an insurmountable one.

The Walled Garden of SoFi

SoFi is building a walled garden of financial services, and with each new product released, the walls grow higher, the garden more lush. And within this garden, SoFi unlocked super app superpowers.

Regardless of the hype you might hear about dazzling user experience, AI-driven lending models, or “the global standard in modern card issuing,” financial services are commodities. And the company with the strongest unit economics, wins.

SoFi’s super app invokes the strongest economics of any financial services company in the free world, and this advantage will gradually suffocate the fintechs that did not take steps to broaden their offerings. Today’s diversification discounts will become diversification premiums.

With the banking charter, SoFi will be able to charge less for loans, offer more to members for deposits, and still come out making more than competitors. Through Galileo, SoFi transmutes R&D costs into software revenue, sending tendrils of ubiquity into each and every corner of the fintech revolution. And between SoFi Stadium and Noto’s masterclass in viral marketing, SoFi is redefining customer acquisition metrics.

As we look out into the dimly lit expanse of 2022’s unknown and beyond, I hope this article is a welcome light for the future of finance and SoFi’s critical role within it. A beacon to remind you growth is opportunity, after all, and the discounts of December will not last forever.

Where we are going we don’t need roads, but we’ll still find SoFi there.

The bank of the future.

Stay convicted.

Tyler

Huge thanks to you, noble reader, for staying with me until the end of this piece. If you liked the article, please click the below buttons and share with your friends/family/followers. I truly appreciate your support and feedback. 🤓

As always, feel free to find me on Twitter to let me know what you liked and what you didn’t about this post.

Congratulations from Spain. I found your blog by very coincidence. Very good review. I really liked it and appreciate your effort. I happened to buy the Sofi stock at 18$ but i went out at 22.27$ because I couldn't understand it fully. Now it's so cheap and your report is so clear. Thanks a lot!

Fantastic article